Attractive UBI Business Models for US Consumers

By Thomas Hallauer

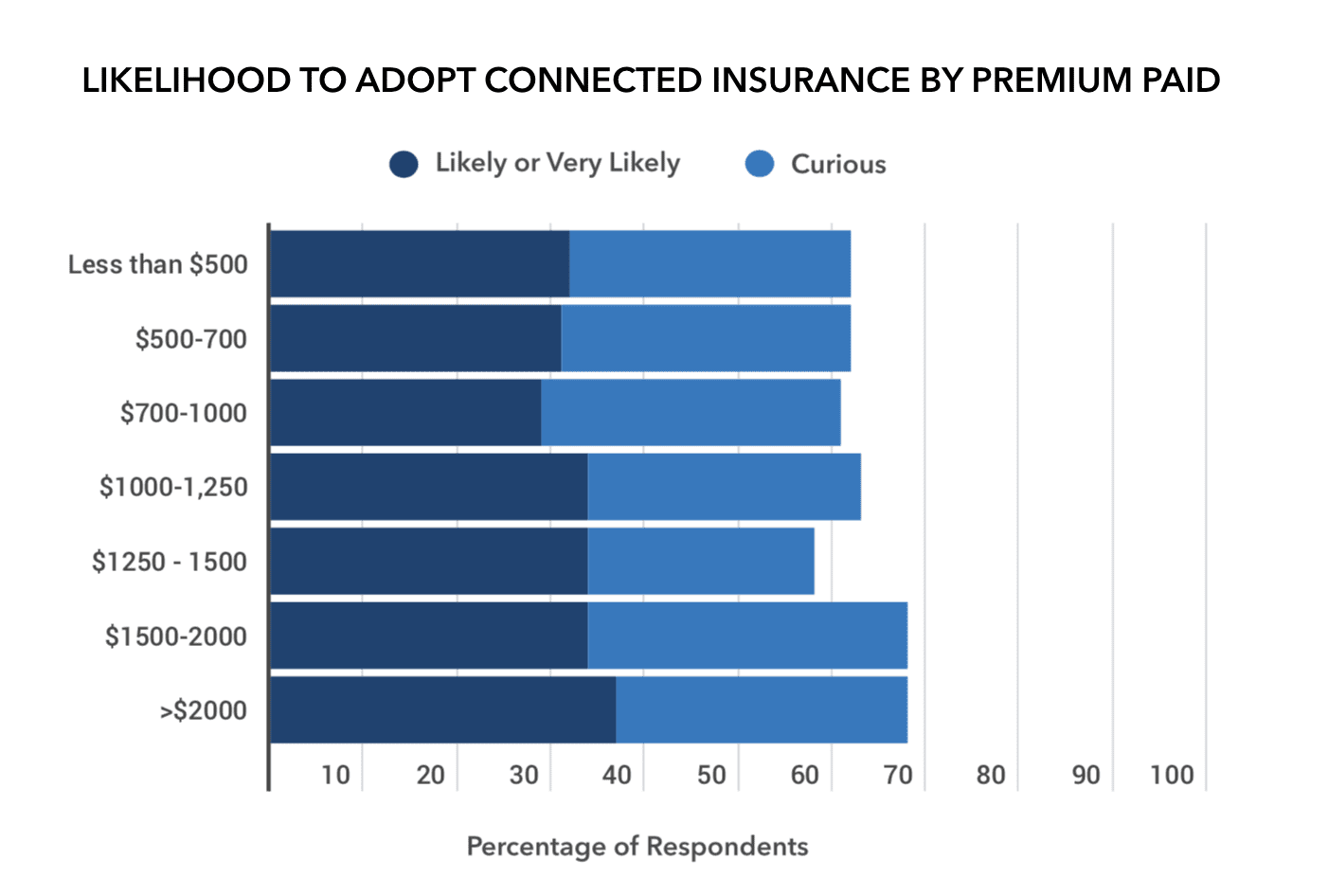

This month, CMT released a large report entitled Attractive UBI Business Models for US Consumers, based on a series of surveys conducted over the last two years. You may already have seen the headline: 63 percent of U.S. drivers are ready to switch insurance coverage. The value proposition they want from their insurers is telematics-based, mobile, and enriched with services.

Looking past the headline, and you will see the whole report is critical for three reasons:

Many of the past insurance programs have failed because they put technological and actuarial benefits first. They had transformed the UBI proposition into a barter of data against discounts. As a result, telematics became a necessity for young drivers to afford insurance. One of the biggest opportunities – reducing risk by rewarding driving behavior improvement – was initially overlooked.

The story has now changed, and the study demonstrates how driver demand is moving the value proposition to safety-centric benefits with telematics as the key enabler.

Nothing happens overnight in the insurance sector. As Matteo Carbone mentioned: ”In all these years, I have come to realize telematics is an enabler of new business processes. It doesn’t create value per se. Any insurance telematics program is designed to fail if it is not part of a business strategy and if the definition of this strategy is not driven by insurance functions.’

Some insurers still resist change and until recently thought telematics value propositions didn’t bring enough to warrant a serious look. COVID has changed that in a dramatic way. Competing in auto insurance today requires at least to match with the competition on connected offerings. To win, insurers need to understand what model will attract new customers – and that’s the goal of this report.

Finally, as local governments began to react to the virus by locking down cities and states, normal driving patterns disappeared. By the third week of March, morning and afternoon rush hours were gone. But while quarantines have started to soften, the traffic jams have come back slowly and during different times of the day. Commuters are using their vehicles differently and there is no clear indication if or when things will return to “normal”. As a result, previous risk models for commuters are rendered unusable; without individual driver data, insurers’ traditional risk proxies are no longer predictive.

On top of that, carriers have been forced to distribute cashback in compensation for the drop in driving during the lockdown. Finding the right value proposition to make individual, behavior-based insurance attractive has now become vital.

We believe these factors should at least pique the interest of insurers enough to explore Attractive UBI Business Models for US Consumers. Also, this research into consumer sentiment in the United States contains real actionable insights for insurers looking to expand their books of business through connected insurance.