Why UBI is trending toward continuous programs

By Ryan McMahon, CMT’s VP of Strategy

This article first appeared on Digital Insurance.

I’m sure this story will resonate with many of you in the industry: Your friends learn that you work in the insurance industry, and they start asking you every possible insurance-related question that they can think of. You may be a commercial property pricing actuary or an inland marine underwriter — but with friends seeking help on their personal auto or home policies.

This was the position I was in with a friend of mine, Alex, before the pandemic. Alex had not demonstrated that he is a safe driver in the past — he has a number of speeding tickets and an at-fault accident. Alex pays well above the national average for his auto policy. He came to me to ask how he could save money on his insurance bill. He had already gotten quotes from a number of carriers, yet he was not offered a telematics policy — despite asking to save the most money possible.

I suggested that Alex call the companies he got quotes from and ask specifically for a telematics-based auto insurance policy. J.D. Power reports that when consumers are offered a telematics based policy, the take rate is 49 percent. The industry can benefit from making more offers.

After getting the telematics-based quote, Alex decided to enroll in a behavior-based insurance policy. While Alex didn’t have a clean driving record, he had developed to a safer driver. He followed the program instructions, installed the app, and drove safely for 90 days — speeding less and keeping his focus on the road. He earned a safe driving discount of 15 percent starting in February 2020. He’ll have that discount for the life of the policy. He was happy with the result.

After COVID-19 silenced the nation’s roads in March 2020, Alex was lucky and was able to work from home during that period. But in early May, Alex hit the roads again. Unfortunately, his driving became riskier. I noticed that Alex was using his phone more while driving and he was driving faster than I was comfortable with. He had already finished his 90-day monitoring period, so his auto insurer didn’t know about these risky behaviors. His safe driving discount stayed the same — despite his higher risk.

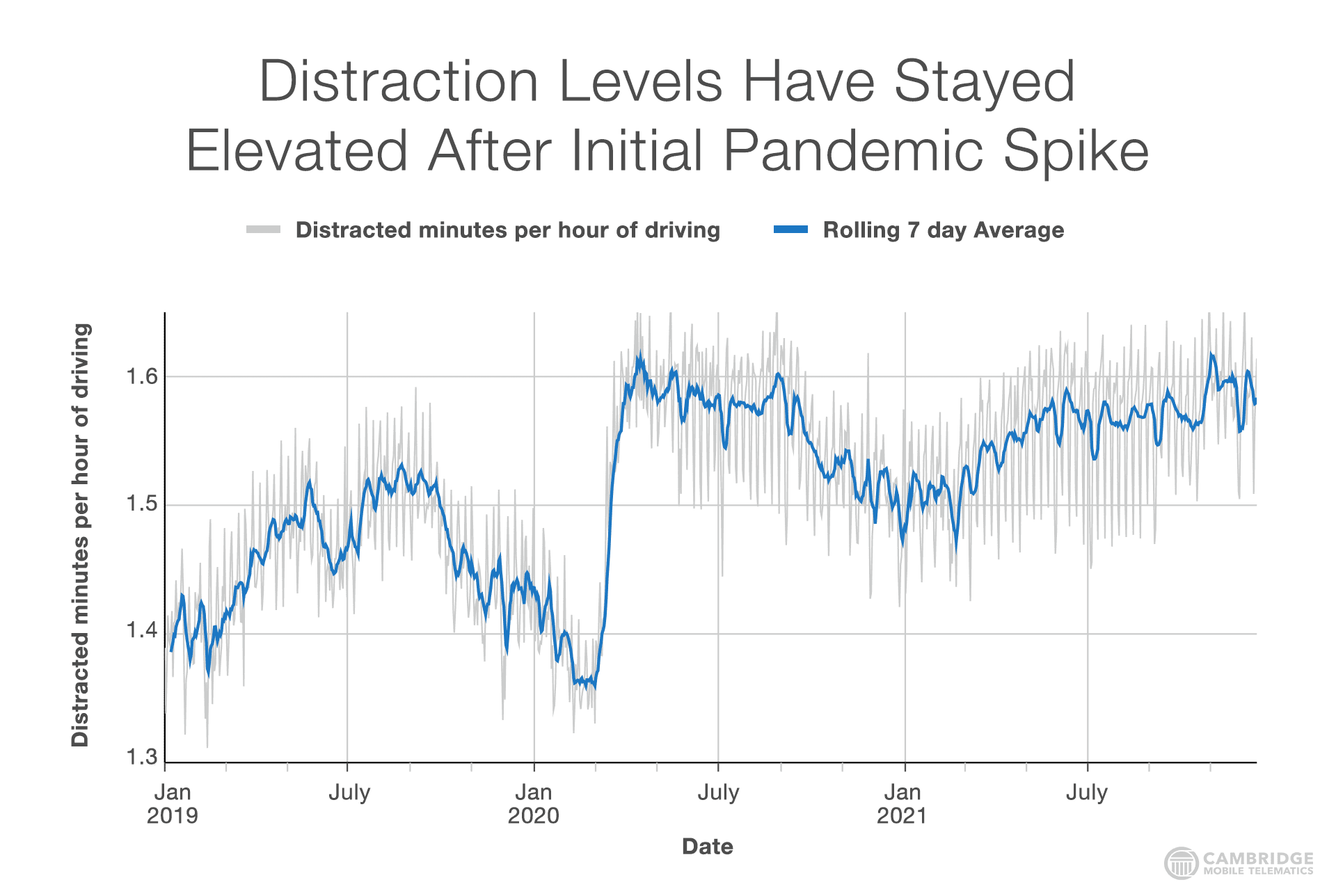

Alex’s story is the same for millions of Americans in the post-pandemic era. As roads opened up, speeding increased, distracted driving increased, and risk surged. CMT data shows that speeding jumped over 50 percent and still hasn’t returned to pre-pandemic levels. CMT data shows a similar trend for distracted driving. As of December 15th, Americans were still spending an average of 9.8 percent more time driving distracted than the year before the pandemic.

What’s interesting though, is not all drivers got worse. In fact, long-term telematics users stayed roughly the same in exhibited risk over the course of the pandemic. Transient drivers who came in and out of telematics programs showed the highest level of risk variability.

As Alex’s story shows, the time-limited UBI monitoring period leaves insurers exposed to two kinds of risk. The first is environmental, like COVID, where societal conditions change driving behaviors. The second is behavioral, where people drive safely while monitored but revert to risky behaviors once they lock in their discount.

The exposed risks from time-limited monitoring programs create segmentation challenges for insurers and removes the opportunity for long-term driver coaching. The strategic advantage telematics programs like UBI provide is that they enable insurers to segment risk at more granular levels than traditional variables. Risky behaviors invisible to insurers with traditional variables are easy to identify and assess with telematics. Insurers can offer more personalized pricing for every customer. They can keep their best customers with better pricing and adjust pricing for riskier drivers or coach them to improve. With time-limited monitoring periods, an insurer has a specific timeframe to segment and improve a driver’s behavior. After that, the window closes.

The good news is that insurers don’t need to be exposed to environmental or “best behavior” risk anymore. The time-limited monitoring period is a remnant of the hardware days when insurers balanced expensive hardware costs with program profitability. Today, auto insurers use inexpensive IoT devices and smartphones to capture granular driving behaviors.

Top insurers are already investing in these technologies to scale their telematics programs and grow profitability. Seven of the top 10 insurers have adopted a continuous monitoring strategy to accelerate growth. Travelers recently announced that its IntelliDrive program grew 50% last year. To capitalize on this growth, Travelers has introduced IntelliDrivePlus, a continuous program.

USAA, which also offers a continuous program with SafePilot, announced in September that “daily driver enrollment year-to-date is 203 percent higher than in 2020… [with] almost half of new policyholders opting into the program.” If you watched Monday Night Football this year, you know USAA invested heavily in TV advertising to increase awareness for SafePilot.

Beyond continuous safe driving discounts, Farmers Insurance has created always-on value propositions for customers. It offers a monthly rewards program for active Signal users based on “focus time.” Farmers also offers a free crash assistance program where its Signal app can detect when a customer crashes and dispatch an ambulance. If you’ve watched much TV over the past six months, you’ve probably seen Farmers ads for the Signal program and the crash assistance feature. (Farmers, Travelers, and USAA are CMT clients).

As you can see, top insurers have embraced a continuous strategy not just to avoid environmental and “best behavior” risk, but to increase value for customers and customer engagement and retention. For example, CMT data shows that rewards programs increase customer engagement. We’ve seen rewards programs that drive customers to engage their telematics app 12 times a week. For comparison, customers open the typical insurance app only one to two times per quarter.

Car crash assistance programs are among the most popular products for insurance customers today. Many top insurers build their crash assistance offering directly into their telematics app with continuous monitoring. Beyond the benefits of proactive crash support for customers and downstream improvements in claims operations, these programs work as an additional incentive for customers to keep the app. People love it — the Net Promoter Scores for customers with crash assistance are double the NPS for insurance app users.

The benefits of continuous programs go beyond the features themselves. With continuous data-driven features like UBI, rewards, and crash assistance, insurers can personalize their communications with customers. They can congratulate them when they drive safely, nudge them in the right direction when they’re risky, and remind them they’re protected on the road. All of these engagements deepen the customer relationship.

A continuous program could also help improve top-of-funnel conversion rates. Continuous monitoring can de-risk behavior-based models for customers concerned about increased rates. Instead of having one shot at earning their safe driving discount, they can focus on improving in the next term.

Perhaps most importantly, continuous programs continue to incentivize safe driving because you have to “earn” your discount every term. Think about my friend Alex. Instead of getting a 28% discount for the life of his policy and going back to his risky behaviors, a continuous program would have educated him on the impact of his speeding and distraction during COVID. His discount would have been in jeopardy. Perhaps he would be a safer driver today.

This speaks to the larger point: Continuous programs are a win for everyone. They’re a win for society because they incentivize safer driving, so roads are safer and there are fewer fatalities. They’re a win for consumers because they always have the opportunity to get the lowest rate. And, they’re a win for insurers because they help better price and reduce risk, and build a stronger competitive advantage. Expect them to be the standard for telematics programs from now on.